Real interest rates are negative at the moment. By keeping them this way, the RBA is encouraging spending, facilitating the transfer of wealth from savers to borrowers and causing malinvestment.

That may seem to be a lot to unpack – but economics isn’t hard. Yes, there are people who are paid to make it look hard but let me step you through negative real interest rates, what that means for consumers and investors, and why it means further rate rises are inevitable.

The real interest rate is the nominal rate of interest (the one you see on your bank statement or in the paper) less the rate of inflation.

Right now, the RBA’s nominal cash rate is 3.5%. Deduct CPI at 7.0% and the result is a real official interest rate of negative 3.5%.

Let’s clarify the key terms in this equation.

The “nominal interest rate” is the interest rate that you pay – the price of your money reported by banks and discussed by media.

For the purposes of discussion, let’s assume we are lending to the Australian government and so we will use the “Cash Target Rate” as published by the RBA – 3.5%.

Now let’s consider inflation. In a previous article I explained the Austrian School of Economics definition of inflation: an expansion in the supply of money through money printing, government debt and deficit spending. Higher prices are the eventual consequence of inflation.

The commonly accepted measure of inflation in Australia is the Consumer Price Index (CPI) – which is currently 7.0% as most recently published by the RBA.

But let’s make this “real world” – Westpac is offering 4.25% on term deposits. So that’s a real interest rate for savers of minus 2.75%. Westpac is also offering home loans at 4.9% – a real interest rate for borrowers of minus 2.1%.

If the bank is offering to pay you -2.75% on your savings, or lend you money at -2.1% – what do you do?

Why are these numbers important? Lenders set interest rates so that when they get paid back at some point in the future, the money they receive back includes a reward for taking the risk to lend PLUS compensation for any loss of spending power courtesy of inflation.

If I lend you $100 for 12 months today, I need at least $107 back in in 12 months to have the same spending power at that time – assuming you believe price inflation is only the published 7% (who does?).

$107 will not be enough though! I also need to be rewarded with a premium for taking a risk on you. How much this “risk premium” is will depend on the circumstances. Lending to the newly established cafe on an unsecured basis is riskier than lending to the owner of the café secured by a mortgage on his or her house, which is still riskier than lending to BHP, which is riskier than lending to the Federal Government, and so the risk premium increases for each of these accordingly.

Where does the rubber hit the road on this? There are three things you can do with money. You can spend it, you can invest it, or you can save it.

Would you save money

if the money you save

is going to be worth less in 12 months time?

You deposit your money and receive 4.25%, you get your $104.25 back in 12 months time but you can buy less with it then than you can today.

Do you spend it today? If you believe your money is losing spending power, then maybe you will. So now you see, that with rates as high as they are, the current interest rate settings are in fact stimulatory! If the current real interest rates encourage spending and discourage saving, do you think they will work to control inflation or fuel it?

You could invest your money instead of saving or spending it. However, to counteract inflation and preserve the value of savings, investors face the challenge of finding suitable investment avenues. This can lead to the pursuit of high-yield high-risk investments, fostering speculation and malinvestment.

Understanding what interest rates are supposed to do (compensate for lost spending power and risk), the current levels of real interest rates (being negative) make absolutely no sense at all. They punish savers and reward borrowers, effectively transferring wealth from the former to the latter. And they encourage investors to jeopardise their wealth by seeking risk.

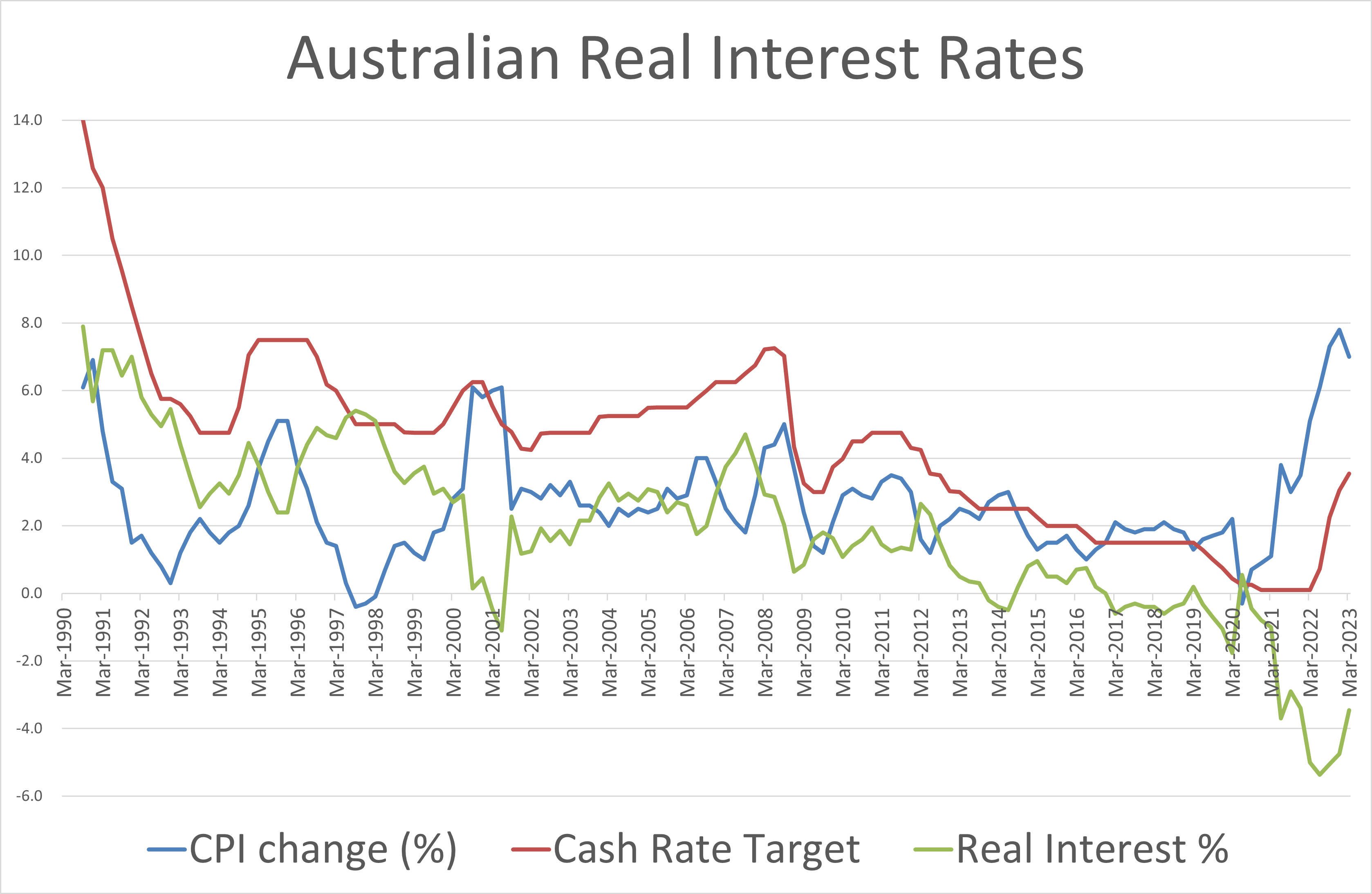

Where are interest rates headed then? Take a look at the chart below. Historically the Cash Rate Target tracks above the CPI – for the reasons explained above. And real interest rates are historically positive.

When observing this chart, can we really believe interest rates have peaked? That the RBA won’t be lifting interest rates again – if not tomorrow then certainly in coming months. And again and again?

Thank you for your support. To help us in our battle to protect liberty and freedom please click here

Nicholas Samios is a fund manager and small business investor with a wealth of experience spanning three decades in commercial finance and SME capital raising. In his spare time, he puts on his “Austrian School” economist hat and utilises his insights from the commercial

world to analyse the economic landscape for SMEs and entrepreneurs.

")

{kind=link}